A Subtle Shift to a Higher Tax World

Under last year’s One Big, Beautiful Bill Act (OBBBA), Congress preserved the seven familiar income tax brackets. On the surface, it feels like nothing really changed.

But just beneath that surface, something important did change. New deductions and targeted relief provisions were added, and many of them gradually phase out as income rises, especially for those with incomes between $100,000 and $500,000.

The result is subtle, but meaningful: many households now experience higher effective tax rates than their stated bracket might suggest.

Read More: What's My 2026 Tax Bracket?

Marginal Tax Brackets Versus Real Life

Most people think about taxes in terms of brackets. “I’m in the 12% bracket” or “I’m in the 22% bracket.”

That’s a helpful starting point, but it’s only part of the story.

What really matters for good planning is what happens to your next dollar of income. In other words, your effective marginal tax rate.

OBBBA introduced and expanded several income-based benefits, including the enhanced senior deductions and targeted SALT relief. As income increases, these benefits gradually phase out. When they do, the loss of deductions behaves like an additional tax.

You may still see a 12% or 22% bracket on paper. But your next dollar of income may be taxed more like 24%, or even higher.

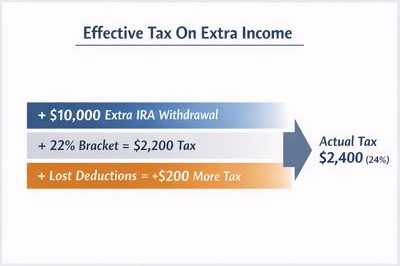

For example, in 2026, a married retiree making $100,000 of taxable income is in the 22% bracket. Suppose they decide to take an extra $10,000 IRA distribution to fund a project. On paper, that $10,000 should cost $2,200 in federal tax. Instead, the additional income causes a partial loss of enhanced senior deductions. The tax bill rises by closer to $2,400.

That extra $200 is not shown as a “tax rate” anywhere. It is the silent cost of lost deductions. The effective rate on that $10,000 is now closer to 24%. That extra $200 difference doesn’t show up on a tax table, but it’s very real.

Thankfully, the extra cost is manageable with the right awareness and planning.

A Familiar Pattern in the Tax Code

This approach isn’t new. It reflects a long-standing pattern in how tax policy evolves.

- Before 1984, Social Security benefits were not taxed. Now they are.

- Before 2007, Medicare IRMAA surcharges did not exist. Now "IRMAA" is a household name.

- Before 2013, the 3.8% Net Investment Income Tax was not in place. Now it looms.

Rather than raising headline tax rates, Congress has often adjusted the system through income-based thresholds and phaseouts.

OBBBA continues that trend. The bracket structure remains familiar, but the underlying mechanics reward more thoughtful planning.

Good Tax Planning Matters More Than Ever

Retirees are especially likely to encounter this higher tax dynamic, not because something is going wrong, but because they often have multiple income streams working together.

As income sources layer together, the impact is gradual rather than dramatic. Pension or portfolio income stacks on top of Required Minimum Distributions and Social Security benefits. One-time events like Roth conversions or a home sale push income higher. There’s no flashing warning sign, just a quiet shifting of how each additional dollar is treated.

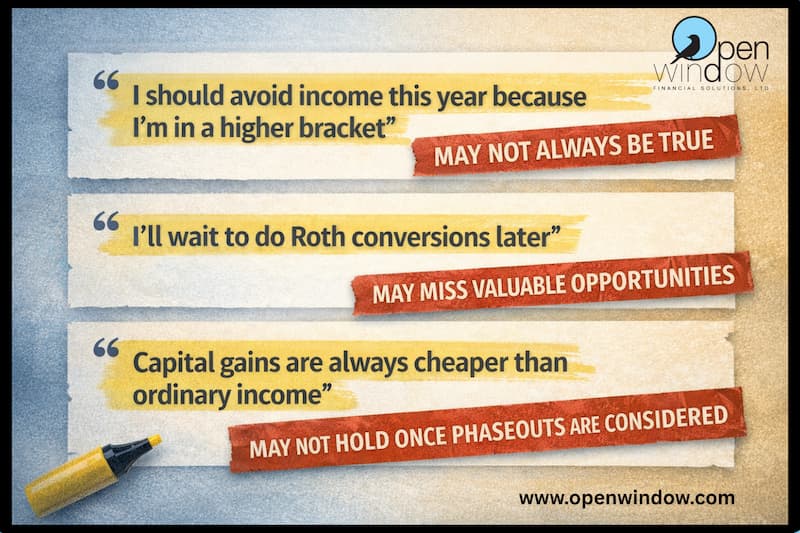

When effective tax rates become more dynamic, simple rules of thumb become less reliable.

The goal shifts from minimizing income in any single year to managing income over time, which can mean:

- Recognizing income earlier, while rates are more favorable

- Spreading income across multiple years

- Paying a known tax today to avoid a potentially higher one later

Perhaps most counterintuitive of all, there are times when intentionally realizing more income can actually lead to a lower overall tax burden. That’s not a loophole. It’s a reflection of how the system is now designed.

The Takeaway

Tax brackets may look the same, but the planning landscape has evolved.

The good news is that this shift is navigable. With a clear understanding of how today’s rules interact, it’s possible to make more confident, informed decisions.

Two retirees with identical taxable income can experience very different outcomes depending on how that income is sourced, timed, and coordinated. One plans proactively and stays in control of key thresholds. The other simply follows the default path. On paper, they look the same. In practice, their tax experiences can be quite different.

At Open Window, helping clients navigate these kinds of subtle but important shifts is exactly what we do. With the right strategy, what feels complex can become a source of clarity and confidence.

If we can help you think through your situation, reach out at (775) 827-0670 or schedule a 'Quick Connection' at www.openwindow.com/connection.