Navigating "530A" Accounts

|

Key Takeaways

|

July 4, 2026, marks the planned launch of a new savings and investment vehicle for children. Created under the "One Big Beautiful Bill Act (OBBBA)" and called Section 530A accounts, these accounts are designed to help families begin long-term investing for children from an early age.

We view these accounts as a hybrid between a traditional IRA and a custodial account, offering early tax-advantaged growth without requiring a child to have earned income.

While some details are still being finalized, enough is known to evaluate where these accounts may fit within a family's broader planning strategy.

530As: A Unique Hybrid

The defining feature of a 530A account is that a child does not need earned income to participate.

| Feature | 530A | 529 Plan | IRA / Roth IRA |

| Earned income required | No | No | Yes |

| Tax-advantaged growth | Yes | Yes | Yes |

| Education restrictions | No | Yes | No |

| Available before age 18 | No | Yes | Yes |

| Federal seed contribution | Yes | No | No |

530As address a longstanding gap in children's savings options. Custodial accounts allow families to invest on behalf of a child, but generally create taxable income. 529 plans offer valuable tax benefits but are intended primarily for education expenses. Traditional and Roth IRAs provide tax advantages but require earned income. 530A accounts are designed to bridge that gap.

Like a custodial account, a 530A is owned by the child and managed by an adult until age 18. Unlike a 529 plan, however, the account is intended as a long-term savings vehicle rather than an education-focused account.

530As allow families to begin tax-advantaged compounding for a child as early as the day they are born.

We do not view 530As as a replacement for 529 plans, which remain the standard tool for education funding when pursued early in the child's life. Rather, 530As may serve as a complementary tool, a starter-IRA for families interested in creating a long-term retirement asset for a child.

The "Seed" Contribution Opportunity

One of the most compelling features of the legislation is the proposed federal seed contribution.

Children born between January 1, 2025, and December 31, 2028, are eligible for a one-time federal contribution of $1,000 to be deposited directly into a 530A.

In addition, up to 25 million children age 10 or younger who live in zip codes with median incomes below $150,000 may receive a separate $250 deposit through a charitable contribution from the Michael & Susan Dell Foundation.

For eligible families, opening a 530A account seems to provide an opportunity to capture this initial funding and establish a meaningful head start on long-term savings.

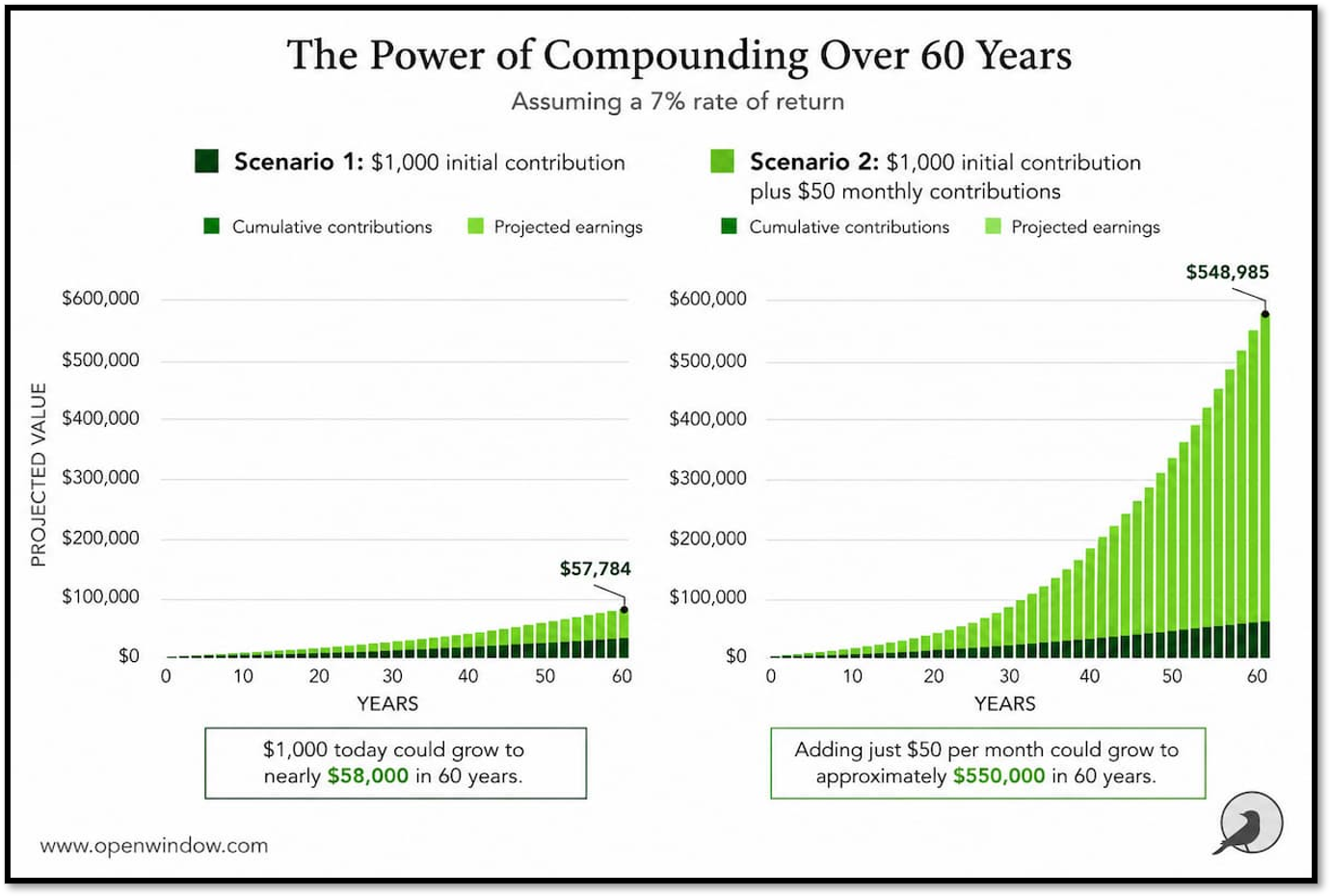

To illustrate the potential impact of compounding, a $1,000 contribution growing at 7% annually could reach nearly $58,000 over 60 years. Adding just $50 per month could increase the projected value to approximately $550,000 over the same 60-year period.

How Do 530A Accounts Work?

While some aspects of 530A accounts—sometimes referred to as "Trump Accounts"— are still in flux, the broad framework is becoming clearer.

Eligibility

Accounts are available to minor children. The child must be a U.S. citizen with a Social Security number and under age 18 on December 31 of the year the account is opened.

Account Opening

Accounts must be opened and managed by a guardian → parent → adult sibling → grandparent. The legislation specifies that account opening should follow this hierarchy, meaning that a grandparent generally would not be able to open and manage the account if a parent, guardian, or adult sibling is available and willing to do so.

Accounts can be opened in several ways:

- Accounts can be opened by filing IRS Form 4547 with your annual tax return.

- Accounts can be opened on the secure IRS website, "IOLA," at www.IRS.gov/payments/online-account-for-individuals. The IRS's IOLA website also requires an initial hurdle of creating an ID.me account to verify your identity. Once verified and logged in, click the "Menu" option, then select "Forms," and then select "Trump Accounts" to begin the account-opening process.

- Accounts can be opened at www.trumpaccount.com. If visiting the website on a mobile device, you will be directed to an official app sponsored by the U.S. Department of the Treasury that guides you through opening an account. A bit of confusion is likely here, given that the government's own website marketing the accounts (www.trumpaccounts.gov) uses the plural "trumpaccounts" and is a "dot gov" address, while the website to sign up (www.trumpaccount.com) uses the singular "trumpaccount" and is a "dot com" address.

No matter the route you take to open an account, once it's processed, the federal government will email you instructions and links to open the actual 530A account.

Once finally opened, the account is expected to be administered through a designated custodian. Currently, these designated custodians include BNY Mellon and Robinhood.

Contributions

Annual contributions are limited to $5,000 per child. Any adult can contribute to a child's 530A.

Employers may provide annual matching contributions of up to $2,500 per employee, with those contributions counting toward the annual $5,000 limit.

The potential $1,000 government seed contribution does not count toward the annual $5,000 limit, nor do other potential contributions by states, local governments, and 501(c)(3) charities.

Tax Treatment

Individual contributions are generally made with after-tax dollars (not tax-deductible). Said another way, individual contributions are expected to create a basis within the account that will likely need to be tracked on Form 8606.

Employer contributions are treated differently and are expected to be taxable upon withdrawal.

No matter who made the contribution, growth and earnings inside the account are tax-deferred and then become taxable as ordinary income when withdrawn.

Growth Period

From account opening until age 18, assets are generally locked and cannot be accessed.

During this period, investments are limited to a menu of low-cost, broadly diversified index mutual funds or ETFs.

One subtle but fascinating aspect of 530A accounts is that they represent one of the federal government's clearest endorsements of long-term, market-based investing for everyday Americans. Unlike Social Security, whose trust funds are invested almost entirely in Treasury securities, 530A assets participate directly in the growth of the stock market through diversified index funds and ETFs. The program's greatest test will likely come during its first major bear market decline. Fortunately, because withdrawals generally aren't permitted until age 18, families are naturally encouraged to practice one of the most important disciplines in successful broad market investing: staying invested through periods of uncertainty and allowing compounding to do its work.

Access Period

Beginning at age 18, the beneficiary gains full control of the account.

At that point, they can maintain the account, transfer into a Traditional IRA, or pay taxes and take withdrawals or convert assets over to a Roth IRA.

Beginning that same year, the account resembles a traditional IRA, including a potential 10% penalty for withdrawals before age 59 ½ unless an exception applies—such as certain education expenses, first-time home purchase (up to $10,000), birth or adoption costs (up to $5,000), qualifying medical expenses, disability, or terminal illness.

Tax-Aware Nuances of 530As

While the federal tax treatment offers tax-deferred growth, there are critical tax-aware details that must be managed.

State-Level Taxation

Although the accounts receive favorable federal tax treatment, some states may continue to tax annual account growth.

Several states currently plan to tax the annual growth of these accounts like a regular taxable account. Families living in states such as California, Hawaii, Kentucky, Massachusetts, Pennsylvania, South Carolina, and Wisconsin should pay particular attention to evolving guidance.

Basis Tracking

Because individual contributions, employer contributions, government seed contributions, and investment earnings may receive different tax treatment, accurate "basis" tracking on Form 8606 will likley be important to avoid unintended double taxation.

Gift Tax Considerations

Gift tax treatment was one of the biggest unanswered questions surrounding 530A accounts leading up to their July 4 launch.

Until June 30, 2026, many practitioners interpreted contributions to 530A accounts as "future interest" gifts that might not qualify for the annual gift tax exclusion, potentially requiring the filing of a Form 709 gift tax return. Less than 24 hours before this article was published, however, the IRS released guidance clarifying that contributions to a 530A account generally qualify as present-interest gifts eligible for the annual gift tax exclusion. As a result, a contribution to a 530A account, by itself, generally does not require the filing of a Form 709 gift tax return. Unfortunately, more clarification is needed, as a gift tax return may still be required if the donor makes other gifts that independently trigger a filing requirement.

This episode highlights how quickly the guidance surrounding these new accounts continues to evolve. While the IRS resolved one of the most significant open questions, several others remain. We expect additional clarification in the weeks and months ahead. Until then, families considering substantial contributions may wish to discuss their funding strategy with their advisor. In some situations, gifting cash directly to the child (within the annual exclusion amount), who then contributes those funds to the 530A account, may provide an additional layer of simplicity while guidance continues to develop.

Caution on Roth Conversions

Many families are understandably interested in the possibility of converting 530A assets to Roth IRA when a child turns 18.

Before proceeding, be aware how the “Kiddie Tax” can apply to these conversions for students up to age 24, which can blunt the tax benefits by taxing the conversion at the parents' higher income tax rate.

Open Window's Perspective

The behavioral design of 530A accounts may ultimately prove to be one of their greatest strengths.

The combination of mandatory low-cost, diversified investments, a very long investment horizon, and virtually no ability to sell during periods of heightened uncertainty creates an environment that naturally encourages successful investing behavior.

For many families, we expect 530A accounts to serve as a valuable complement—not a replacement—for existing planning strategies.

We continue to view 529 plans as the preferred vehicle for education funding, while Roth IRAs remain the gold standard for retirement savings when a child has earned income. However, for families wishing to establish a long-term investment asset for a child from an early age, 530A accounts appear to fill an important gap.

For all families with children born between 2025 and 2028, we believe the $1,000 federal seed contribution alone will justify opening an account.

As additional guidance is released, we will continue evaluating how 530A accounts fit alongside 529 plans, Roth IRAs, and broader family wealth-planning strategies. Our expectation is that, for many families, they will become another useful tool in a well-designed financial plan.

Next Steps

530As represent an opportunity to help build a stronger, more flexible financial foundation for a child. These accounts can work in tandem with other savings vehicles such as 529 plans and IRAs to give children a financial leg up.

If you are considering a 530A account, we suggest:

- Identifying eligible children born during the 2025–2028 eligibility window and opening an account once administrative procedures become available to capture the federal seed money.

- Evaluating how a 530A account fits alongside existing 529 and retirement savings strategies.

- Reviewing employer benefits for potential matching opportunities.

If you'd like help determining whether a 530A account aligns with your family's goals, contact your Open Window advisory team. We'd be happy to help evaluate whether this new planning tool fits within your broader financial strategy.

Reach out anytime at (775) 827-0670 or schedule a Quick Connection time at www.openwindow.com/connection.