Are You Getting Killed On Taxes? Myths & Tips

A tax-aware understanding of your finances is essential to preserving and growing wealth, regardless of age, income level, or stage of life.

Each year, we see high earners and disciplined savers overpay simply because they misunderstand how the system works. Then tax laws change. Rates shift. Opportunities expire. No wonder so many mistakes are made! Yet, surprisingly, most of the damage is not caused by complexity. It is caused by persistent myths.

In Don’t Get Killed by Taxes, P. J. DiNuzzo and Steven Jarvis outline several of these myths. With permission, we are sharing a few, along with our perspective on how to approach them thoughtfully.

Tax Planning Myths:

Myth: There’s nothing I can do about the amount of tax I owe

The tax code is filled with choices.

Withholding levels. Filing status. Retirement account selection. Business structure. Timing of income and deductions. Investment location. Roth conversions. The list goes on.

Inaction is also a choice, and often the most expensive one.

Myth: There’s nothing I should do about the amount of tax I owe

Taxes fund important public priorities. But there is no reason to unintentionally overpay.

Strategic tax planning is about stewardship. It is about aligning your resources with your family, your intentions, and your values.

Myth: A large refund means I’ve "won" for the year

A refund often means you gave the IRS an interest-free loan.

The goal is not a bigger refund or a zero refund. The goal is to minimize the lifetime tax the IRS keeps while maintaining flexibility and healthy cash flow.

Myth: $1,000,000 in my retirement account means I can spend $1,000,000

Many retirement accounts are tax-deferred, not tax-free.

Traditional 401(k)s, IRAs, and similar accounts create a future tax obligation. In some ways, they function like a loan from the IRS—one where Congress controls the rate. Make sure you understand the tax liability that will eventually come due. Understanding the tax characteristics of each account you own is essential to making realistic retirement income projections.

Myth: It’s too early to think about retirement taxes

Early planning creates optionality. Waiting reduces it.

Many tax opportunities reset annually. If unused, they disappear. The earlier you become intentional, the more flexibility you build.

Myth: I have a CPA, I don’t need a tax planner

A CPA plays a vital role, especially in preparation and compliance.

But preparation is backward-looking. Planning is forward-looking.

Ask yourself:

- Has anyone reviewed your projected tax picture for next year?

- What about the next five to ten years?

- Has anyone estimated your lifetime tax liability?

- Has your strategy been stress-tested against changing tax rates?

If not, you likely have tax preparation, not comprehensive tax planning.

Tax Planning Tips:

Effective planning is proactive. Once December 31 passes, many opportunities for that year are gone.

Good planning identifies opportunities before they expire.

Tip: Look forward, not back

Consider how backward-looking the yearly tradition of Tax Preparation can be. After December 31, your taxes (and your tax bill) are largely set in stone based on actions taken in the year past.

Tax preparation reports what already happened.

Tax planning shapes what happens next.

Forward-looking planning allows you to coordinate income, deductions, investments, and withdrawals in a way that improves long-term outcomes, not just this year’s return.

Tip: Use it, or lose it

Your tax brackets operate on an annual "use it, or lose it" basis.

If you do not fully utilize lower brackets when available, that space disappears permanently.

For some households, it may make sense to intentionally recognize income in lower-rate years rather than defer it indefinitely. This strategy, often called income smoothing, can reduce lifetime tax liability by spreading income more evenly over time.

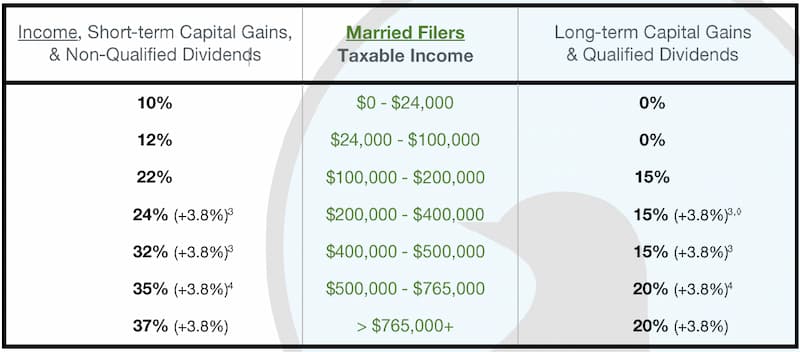

Here are Open Window's Rounded Tax Brackets for married filers.

For more, see What's My 2026 Tax Bracket?

You naturally fill your tax brackets through earnings, pensions, Social Security, and investment income. Think of each bracket as a bucket filling with water.

In the image above, an opportunity exists to fill up the gap in the imaginary 15% bracket. If there is space left, you may have an opportunity.

The key question becomes simple. Would you rather pay tax at today’s known rate or be forced to pay at tomorrow’s unknown rate?

In some cases, intentionally filling a lower bracket today can prevent higher taxation later.

How to "use it": Consider a Roth Conversion

One of the most powerful tools for intentionally using lower tax brackets is the Roth conversion.

A Roth conversion moves funds from a pre-tax retirement account into a Roth account and pays the tax today.

Why consider it?

- Roth assets grow tax-free.

- Qualified withdrawals are tax-free.

- Roth accounts generally have no required minimum distributions for the original owner.

- Roth distributions do not increase taxable income in retirement.

- They can reduce Social Security taxation and Medicare premium surcharges.

- They provide heirs with greater flexibility.

Perhaps most importantly, Roth conversions act as tax insurance by protecting against future rate increases.

Roth conversions are not appropriate for everyone, but they deserve careful evaluation in many cases, including for high earners.

If you’re counting on your tax rate being highest during your highest income-earning years, and lower in retirement, don’t underestimate how Congress can change tax rates with the stroke of a pen.

Read more of our thoughts Here on Roth Conversions and INCOME SMOOTHING.

Tip: Be aware of your silent investment partner, Uncle Sam

Taxes don’t only show up in April.

They show up:

- In asset location decisions (taxable vs. tax-deferred accounts)

- In capital gain realization

- In rebalancing decisions

- In dividend strategies

- In loss harvesting opportunities

An investment strategy that ignores taxes can quietly erode returns. A coordinated tax-wise investment strategy can meaningfully improve after-tax outcomes over time.

Read more of our thoughts here on Tax-Wise Investing.

Tax Planning Is a Long-Term Campaign:

It’s one thing to harness the tips just described. It’s another to make the best use of them.

Tax breaks change. Laws evolve. Life unfolds.

The real value comes not from chasing individual tactics, but from coordinating them into a unified strategy that adapts as circumstances shift.

Tax planning touches nearly every major life transition:

- For retirement

- For high-earners creating tax-free Roths

- For healthcare costs (HSAs)

- For education expenses (529 Plans)

- For charitable givers to help each dollar go further (DAFs)

- For heirs and generational wealth

Effective tax planning reduces friction across these transitions, not just in a single calendar year.

Tax planning is best considered an ongoing campaign staged on multiple fronts over a lifetime, considering:

- Getting a new job

- Buying a home and starting a family

- Selling a home (and possibly trading up)

- Transitioning to a new career

- Taking a leave of absence from work

- Buying or selling a business

- Absorbing the impact of an economic recession

- Sending your children to college

- Selling a home (and possibly trading down)

- Working part-time in retirement (by choice)

- Creating a tailwind for your charitable giving

- Making a life in what we give

- Choosing when to claim Social Security

- Deciphering politics and elections

- Incurring significant health care costs

- Preparing to pass on your wealth and knowledge

Read more OF OUR THOUGHTS HERE on tax planning Techniques.

Weaving Tax Planning Into the Fabric of Your Life

Tax planning requires attention year-round and an awareness of new legislation. Opportunities can be fleeting. Some strategies take years, even decades, to fully realize their benefit.

When done well, tax efficiency becomes embedded in how you save, invest, spend, and give.

We’ve gotten pretty good at building our planning process around this integrated view, avoiding common myths while coordinating thoughtful strategies designed to preserve and grow wealth over a lifetime.

Where Do You Stand?

If you would like clarity on your projected tax path and where opportunities may exist, we are here to help.

ASK US TO SHOW YOU WHERE YOU STAND.

Call the office, send the Open Window team a quick note at www.openwindow.com/quicknote, or schedule a time to talk with Eric at www.openwindow.com/connection.

This piece is provided for information only and is in no way tax advice. While every effort has been made to ensure accuracy, only the IRS tax code itself should be considered official.